Being Right Too Early: Revisiting My 2013 Bitcoin Post on Satoshi’s Forum

What I got right, what I got wrong, and the psychology of timing innovation

Search for a command to run...

What I got right, what I got wrong, and the psychology of timing innovation

No comments yet. Be the first to comment.

Claude-Flow is not another AI coding assistant. It’s a substrate for multi-agent orchestration, built in Rust, and redefining how we build software

A Framework for Product & Organizational Maturity

Real-world lessons on cost, reliability, and developer experience from building production infrastructure at 7Sigma.

AI coding feels magical, until it doesn't. Everyone can now ship a weekend MVP, but when complexity creeps in, the story changes.

“For the vision awaits its appointed time; it hastens to the end - it will not lie. If it seems slow, wait for it; it will surely come; it will not delay.” - Habakkuk 2:3

TL;DR: HODL.

Being right too early is indistinguishable from being wrong, until it isn't.

This is the most expensive lesson of my life - and a hope that others don’t pay the same price.

In December 2013, I outlined an economically grounded case for why Bitcoin could reasonably 40x in value to top cryptographers on the Cryptography Mailing List, in a thread titled [Cryptography] On Security Architecture, The Panopticon, And 'The Law'.

The same Cryptography Mailing List where Satoshi had introduced Bitcoin five years earlier.

At the time, Bitcoin traded around $750, Mt. Gox still ran the market, and mainstream coverage lumped it with Silk Road and scams. Back then, my $31k math sounded insane. Today, it looks conservative, and mainstream analysts now model Bitcoin the same way I laid out in 2013, against M2 Money Supply - not equities, not tulips, not uncorrelated Internet play money.

I came to it honestly. I was an enterprise architect building secure, multi-tenant B2B messaging systems for Fortune 500 companies, living in PKI, encryption, and trust architectures every day. I had also studied economics at UCSD under Mark Machina. Many of my peers from that program went on to defend central banking from the inside. My libertarian leanings sent me the other way.

So when Bitcoin appeared, it hit a trifecta for me: secure and permissionless, supply-capped and outside central banks, and democratized for anyone in the world.

This wasn't just any discussion forum. The Metzdowd Cryptography Mailing List was where the field's luminaries gathered - the people who helped build the Internet's cryptographic rails, exactly the cohort most likely to interrogate Bitcoin's viability with rigor. Several participants in our 2013 discussion have, over the years, been floated as potential Satoshi Nakamoto candidates.

John Kelsey: NIST cryptographer, co-designer of Yarrow and Twofish, author of foundational work on RNGs and hash-function attacks.

Jerry Leichter: Yale computer scientist, expert in distributed systems and cryptography, early contributor to the Linda coordination language.

Ian Grigg: Financial cryptographer, creator of Ricardian contracts and triple-entry accounting, early DigiCash architect.

Phillip Hallam-Baker: Web security pioneer at CERN/MIT, prolific IETF RFC author on HTTP/DNS, introduced the "referer" header.

What followed wasn't much consensus. It was disciplinary lenses colliding: cryptographers reading technical risk and price mechanics, while I argued a money-supply valuation lens. Same object, different instruments.

I had first stumbled across Bitcoin on Reddit a few years earlier, and immediately saw it as revolutionary. To me it wasn't just another form of Internet play money. It was both a monetary experiment and a system with real-world potential - the most exciting humanitarian idea I had come across in my post-college adult life.

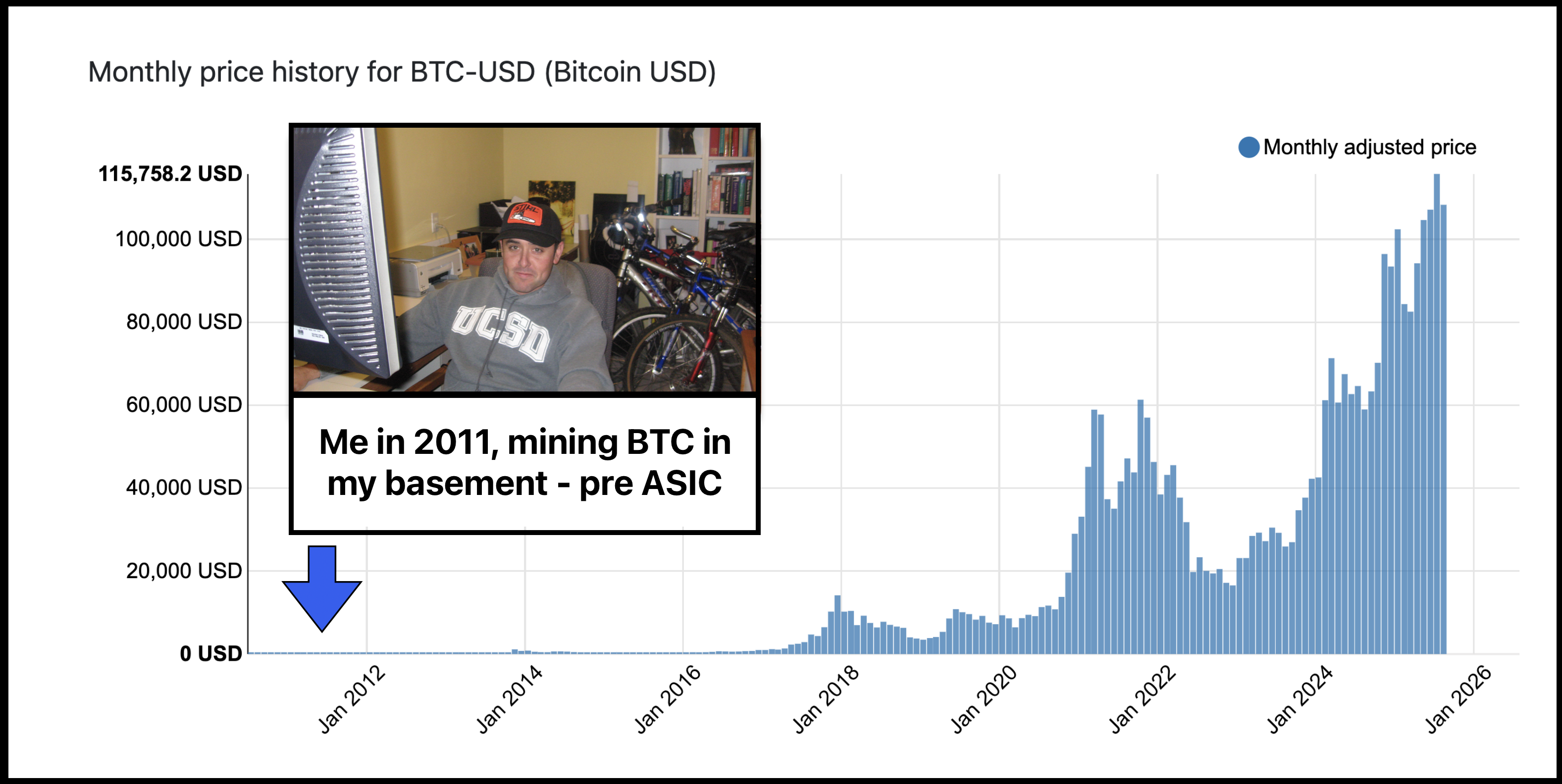

I wanted to understand it concretely. I ran early mining software on a Hewlett-Packard desktop in my basement, met up with like-minded strangers in downtown Seattle to trade small amounts of Bitcoin for cash, used an early peer-to-peer exchange in Finland, and avoided Mt. Gox. I was already buying coffee and sandwiches at a few shops around Seattle - and with the launch of Gyft by mid-2013, I could purchase retail gift cards for Target, Best Buy, and Amazon directly with Bitcoin.

And I was surrounded by a chorus of dismissal: scams, nerd money, too complex, will never be adopted. Even my smartest friends and econ peers laughed it off as a bubble - something only for fools and criminals. By late 2013 the story had shifted: VCs were investing, IBM was experimenting, early adopters like me were buying coffee with it. The frustration wasn’t that everyone was against it anymore; it was that adoption was moving so much slower than the technology warranted. Even five years in, it still felt like the world wasn't ready.

To me, it was the opposite of a scam: a fight against inflationary central banking, and a vehicle for freedom. Seeing something intrinsically beautiful while being told it was tulips or crime was maddening.

Fast Forward to 2013

I had survived the years of outright dismissal, and by 2013 there were finally flickers of recognition. But recognition wasn’t the same as adoption.

Bitcoin had just seen a meteoric climb (beginning the year at $13 and crossing $1000 in November), so when I outlined my stance in December on what I considered common Bitcoin misconceptions, speaking to the cryptographers felt like a chance at the rigorous validation I wasn't getting elsewhere.

I was also an outsider there, having posted only a couple times before. And that's its own hurdle of being early: walking into a room where your credibility isn't yet established, carrying conviction without social proof.

John Kelsey argued Bitcoin would be purchased just-in-time to support online purchases, but made an awful store of value. That economic and monetary framing, he said, simply didn't apply.

I am pretty skeptical that much of the economic theory around monetary inflation or deflation applies very cleanly to bitcoins, given that it's all online, with very low transaction costs, and is likely used only to do specific transactions.

In response to John, and to the broader thread, I laid out sober, economically rooted assertions about viability - including a valuation frame: $31k per coin based on 1% global adoption against M2.

M2 Monetary Supply is 66 trillion. If it all moved to BitCoin, each coin would be worth 3.1 million dollars. If BitCoin saw only a 1% adoption worldwide, each coin would be valued at $31,000 US dollars.

A bubble is 'A theory that security prices rise above their true value and will continue to do so until prices go into free fall and the bubble bursts.' To call it a bubble means that you must have a tangible grasp on its true value. Nobody knows what the true value is. You can’t call it a bubble unless you can identify what its value should be.

It’s very plausible that a second alt coin, possibly an inflationary one, will be used in addition to BitCoin. Where BitCoin would serve as more of a store of value, and an alternate coin would serve as every day cash. In fact, this is already being experimented with today.

People are trying to make sense of something we’ve never seen before in history. This is a new invention. And it is money by definition. There’s no more “if” when you can use it to purchase goods, gamble, and settle debts. We’re already at this point.

In response, Ian Grigg came at it from the opposite end. Where I saw intrinsic value tied to monetary aggregates (macro), he argued that only market price and transaction fees mattered (micro) - that bubble analysis itself was flawed because intrinsic value was unknowable. (Unknowable doesn't mean nonexistent, and it doesn't mean you can't apply first principles to valuing a new innovation.) He nodded more than once at my being an "insider," and therefore talking it up.

In hindsight maybe he was Satoshi, gaslighting us all. 😂

There is no such thing as 'true value' in any measurable or definable sense. There is only price on a market... it's better to talk about today's price if one wants to test economic theories.

One of the symptoms of a bubble is that insiders frequently talk it up :) That's a simple incentives result, there's no reason to believe that insiders have the lock on economic analysis just because they hold BTC.

We could have explored M2 as a falsifiable value proxy; instead my assertion was overlooked.

Meanwhile, Phillip Hallam-Baker was still skeptical, and raised legitimate regulatory concerns - though his comparison to penny stocks and prediction of RICO prosecutions proved overly pessimistic. To his credit, he wasn't wrong to flag regulatory risk; it became the biggest battlefield, exactly as I predicted.

BitCoin is currently indistinguishable from a penny stock in a company that has no revenues, no assets or expectations of any in the future.

Depending on the legal theory the FBI wants to concoct, shutting down BItCoin could be as simple as asserting that everyone who participates in BitCoin in any way is a co-conspirator with the cryptolocker/silk road/etc. organized crime gangs and thus subject to civil forfeiture and criminal prosecution under RICO.

They were each seeing fragments of the puzzle through specialized lenses. Their expertise in cryptography and security was unquestionable, but monetary economics wasn't their domain. And that's where the opportunity lived: in the space between disciplines.

I wasn't predicting "number go up." I was saying "this is money," and framing it against the money supply. To cryptographers, that sounded like bubble talk. To bankers, it sounded like tulips. But to me, it was just math and economics.

Being early demands not just vision, but conviction. Without both, insight can look and feel indistinguishable from error.

Twelve years later, the framing I argued for, Bitcoin in relation to money supply, has gone from fringe island to mainstream.

Academic research now models Bitcoin explicitly against monetary aggregates:

The impact of global economic policy uncertainty on Bitcoin (2023, Journal of International Money and Finance) ScienceDirect

Bitcoin price and money supply (2023, Quantitative Finance & Economics) AIMS Press

Bitcoin Counterflow publishes live charts of Bitcoin vs global M2. Charts

Reddit discussions now track Bitcoin's correlation with global M2, noting it has surpassed gold. Post

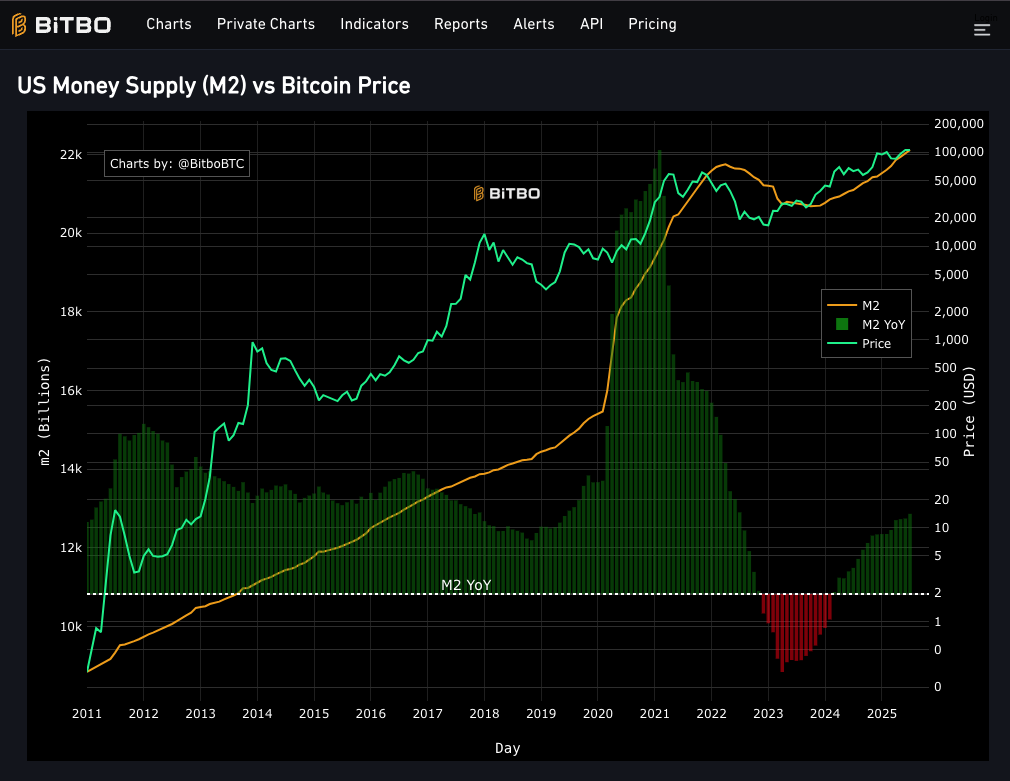

The chart below compares US M2 money supply (yellow) with Bitcoin's price (green, log scale). When M2 expanded, especially during COVID stimulus, Bitcoin surged. When M2 briefly contracted in 2023-24 (a rare event), Bitcoin corrected but held its ground. The rhythm is clear: Bitcoin has been shadowing global liquidity since 2017.

What I framed as simple Econ 101 - "look at money supply, not equities, not digital tulips" - is now a standard analytic lens.

What I Said in 2013 vs What Happened

| 2013 Claim | Reaction Then | Reality by 2025 |

|---|---|---|

| “1% of M2 = $31k Bitcoin.” | Dismissed as delusional; BTC was $750. | Cleared $31k in 2020. Trading ~$110k in 2025. Near 1.7% of global M2. |

| “Bitcoin is money, not a collectible.” | Compared to tulips, Beanie Babies, Silk Road tokens. | Now ETFs, treasuries, and central bank debates. Treated as digital money. |

| “Bitcoin will be store of value; another coin could serve as cash.” | Economists warned hoarding made it useless. | Stablecoins became the “cash.” Bitcoin became digital gold. |

| “Adoption will be exponential.” | Headlines screamed “bubble.” | Survived multiple 80% crashes. Adoption followed an S-curve. |

| “Regulation is the biggest can of worms.” | Barely on governments’ radar. | Became the battlefield: SEC lawsuits, FATF rules, CBDC debates. |

Here's the part that still stings - and the part that matters most.

I didn't HODL.

I had the framework right. I'd anticipated the resilience, the regulatory fights, the valuation. And I still let it fall through my hands, because even though I saw the long-term potential, it felt like not enough of the world believed. Over and over, across cycles, I let social pressure talk me out of my own analysis.

Intellectual conviction is not the same as emotional resilience. HODL and diamond hands aren’t memes - they’re survival skills. It's not enough for an insight to look right on paper; it must survive volatility and human pressure in practice. I underestimated how 80%+ drawdowns would test even a true believer, and how much longer the political battles would last than the technical ones.

I also underestimated timing across the board. Each adoption wave took 3-4 years, not the 1-2 I expected. Paradigm shifts move slower than the frameworks that predict them. But alas, I'm still here. Still building, still innovating.

Document Your Reasoning - Having the original 2013 post allowed for precise retrospective analysis. Predictions without reasoning are just guesses that got lucky.

Quantitative Frameworks Beat Qualitative Opinions - Mathematical models (1% of M2 = $31k) provided testable hypotheses. Numbers create accountability; opinions allow endless revision.

Synthesis Beats Specialization - Cryptographers missed the economics, economists missed the technology. The biggest opportunities live between disciplines.

Skin in the Game Clarifies Thinking - Mining, trading, and using Bitcoin revealed practical realities that theory alone never would. Real stakes force you to confront what you actually believe.

Social Proof is a Terrible Guide for Innovation - When you've done unique work, consensus is backward-looking by definition. Others don't have the context you have - and waiting for them to catch up can cost you everything.

New Paradigms Need New Metrics - Comparing Bitcoin to equities or commodities missed the point. Revolutionary technologies require first-principles analysis.

Adoption Follows Human Psychology, Not Logic - Technical superiority doesn't guarantee adoption. Social proof gates each wave of users.

Being Early Hurts - The gap between right and rich can span years. Conviction without patience leads to capitulation. Sometimes being too early teaches you more than being right.

Looking back twelve years later, the technical predictions held up remarkably well:

Scarcity and network effects made Bitcoin durable

It became the store-of-value, while stablecoins and L2s carried velocity

The network's security has held up, no hacks of the core chain

Politics became the battlefield, exactly as predicted

My valuation math wasn't crazy, $31k was hit and passed

But the real story is human.

Some of my banker friends eventually bought Bitcoin - late, but early enough to profit. I didn't keep my money where my mouth was. I'd correctly anticipated the resilience all along, and still let the chorus of voices turn my conviction into paper hands.

What I missed was the cadence of adoption - expanding circles, each archetype legitimizing it for the next:

cryptography/economics SMEs → libertarian technologists → speculators → VCs → institutions → governments → retirement plans.

And inside each wave, the same emotional cycle played out:

discovery → conviction → doubt → capitulation → reset → renewed belief.

Every crash triggered this sequence. Those who held through - whether from conviction, stubbornness, or simply forgetting their keys - rode the pattern. The "HODL" meme captured something profound about human psychology in the face of volatility.

And each wave of adoption followed the Gandhi arc perfectly:

First they ignore you, then they laugh at you, then they fight you, then you win.

The lesson cuts deep: Being right too early is indistinguishable from being wrong, until it isn't. Trust your synthesis when you see connections others miss. But pair that conviction with patience, because adoption moves in waves, and each wave follows its own psychological cycle.

If Bitcoin has proven anything, it's that the right idea, at the right time, with the right execution, can change the world.

But timing is everything. And sometimes, being too early teaches you more than being right.

I hope this post resonates with anyone who's been early to a paradigm shift, whether in crypto, AI, or any other transformative technology. Too early feels like failure until the world catches up.

Let's see how this post ages in the next 12 years.

Twelve years ago, I saw Bitcoin as money when others saw tulips. I was right about the $31k target, wrong about my own conviction; I was unable to HODL, and it slipped through my hands. Being right too early isn't enough without the execution to see it through.

That's why I built 7Sigma: to turn synthesis into execution, so teams avoid being "right too early" but wrong in practice. We embed at the frontier, where AI reshapes legacy systems, where security meets scale, where paradigm shifts demand more than theory. We don't just predict change; we build through it. Because insights without execution are just expensive lessons.

If these lessons resonate - whether you’re wrestling with adoption curves, navigating regulatory change, or scaling frontier systems - let’s connect.

7Sigma was founded to close the gap between strategy and execution. We partner with companies to shape product, innovation, technology, and teams. Not as outsiders, but as embedded builders.

From fractional CTO roles to co-founding ventures, we bring cross-domain depth: architecture, compliance, AI integration, and system design. We don't add intermediaries. We remove them.

We help organizations move from idea → execution → scale with clarity intact.

Don't scale your team, scale your thinking.

Learn more at 7sigma.io

Authored by: Robert Christian, Founder at 7Sigma © 2025 7Sigma Partners LLC